Table of Contents

showSpending too much on recruitment, payroll or global HR?

We help you find the Best Providers at the lowest cost.

PEO worker compensation involves a PEO managing workers’ compensation claims and insurance for client companies, often reducing risk and cost.

Article roundup

- Workers compensation insurance protects employees in case of work-related injury or illness. It is generally required by law. However, regulations differ from state to state.

- PEOs (Professional Employer Organizations) can provide several HR capabilities to client businesses, including providing and administering workers’ compensation insurance.

- Workers’ compensation insurance through a PEO can be less costly for many small businesses. The PEO is also liable for payments and claims in most circumstances.

- Human error, unclear contracts, or failure of the PEO to provide workers’ compensation insurance meeting state regulations can result in difficulties, liabilities, and even fines to client businesses.

- Potential issues regarding workers’ compensation claims can be avoided by investigating the PEO and their insurer for compliance and thoroughly reviewing the PEO contract.

Working with a PEO can provide different benefits (and potential pitfalls) for many businesses. Businesses in construction, farming, manufacturing, oil drilling, and other industries with a high risk of injury may pursue a PEO partnership primarily because it can offer reduced workers’ compensation insurance premiums and the shouldering of responsibility for workers’ compensation claims.

A PEO (Professional Employer Organization) works with client businesses as a “co-employer”; the client is known as the “workplace employer” while the PEO is the “employer of record.” As the employer of record, the PEO is responsible and liable for employee tax reporting, health insurance and benefits payments and administration, and workers’ compensation insurance coverage. In addition to this, most PEOs offer payroll processing, new employee onboarding, and other packages. A PEO arrangement can provide several benefits for some businesses, however, it is not without potential disadvantages as well.

What is the definition of workers compensation?

Workers compensation insurance is usually required for any company with more than one employee. It is designed to protect workers who suffer from accidents or illnesses as a direct result of their work.

Each state has slightly different laws relating to workers’ compensation payments, which vary according to local regulations. When a worker’s compensation claim is made, it is reviewed by the state’s Workers’ Compensation Board, which decides what payments must be made by the employer’s insurance provider. Payments may consist of weekly cash allowances or cover medical care.

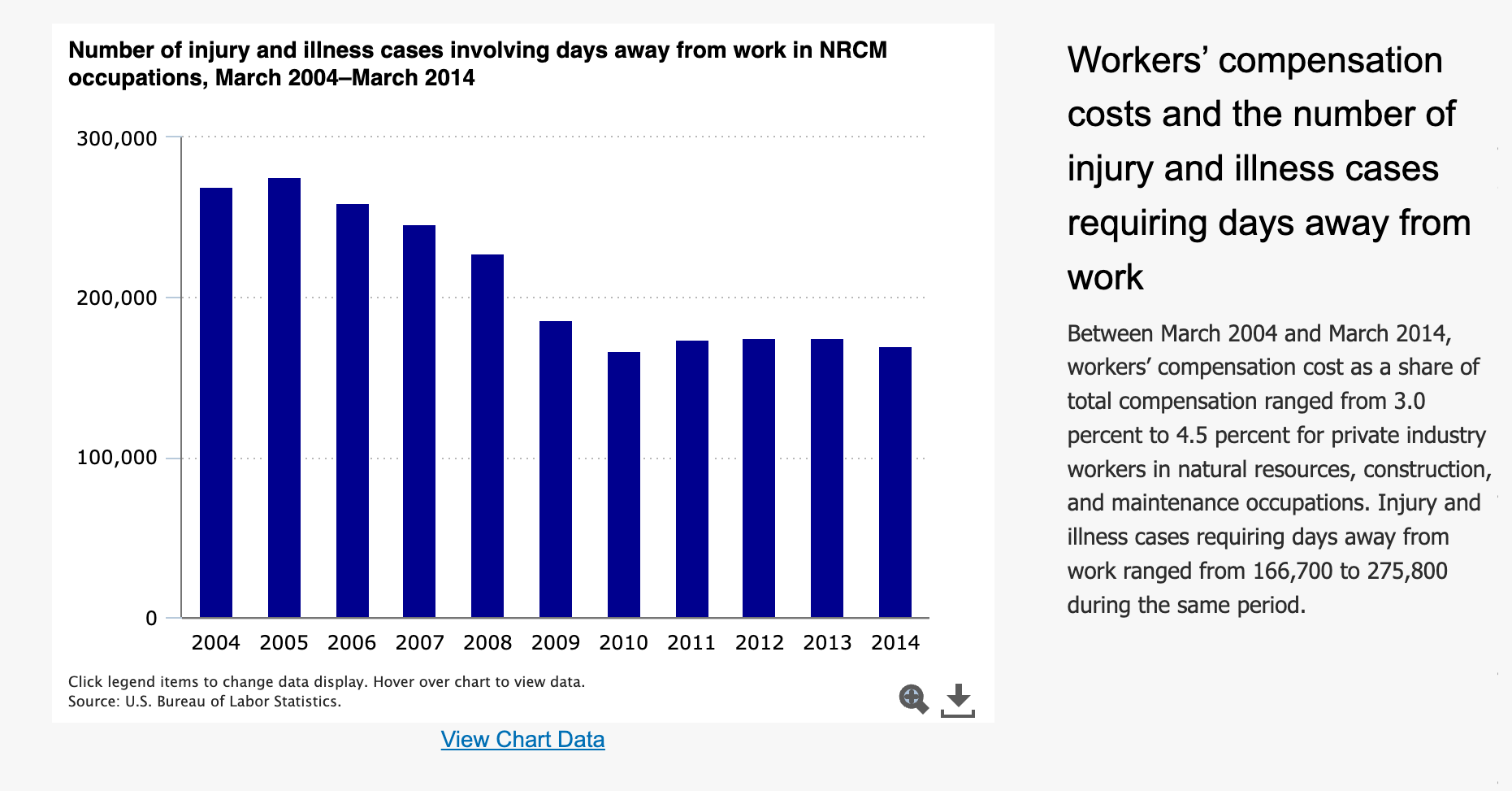

Thankfully, absence due to workplace injuries is especially on the decline — especially in previously high-risk occupations. In the chart below, the Bureau of Labor Statistics shines a spotlight on workplace injury.

While decreasing significant injuries is a good development, everyone must have appropriate workers comp coverage. After all, reduced injury should mean an opportunity for lower premiums.

Can a PEO cover workers’ compensation?

Most PEOs can provide workers’ compensation insurance, health insurance, and other benefits policies.

As the co-employer, the PEO should have a legal workers’ compensation insurance provider recognized by the state where your employees will be working.

What are the benefits of PEO worker’s compensation?

PEOs can generally offer workers’ compensation insurance (and other benefits packages) at lower prices and more stable premiums than those generally provided by insurers to small businesses.

A PEO is a co-employer with several businesses comprising thousands of staff. PEOs thus offer insurers a significant “risk pool”; this means that the number of employees who will potentially make a worker’s compensation claim is a relatively low percentage of the total staff. If a company of 10,000 employees files one claim, the company as a whole costs the insurance company less than a company of 100 that files one claim.

The high-risk pool of a PEO allows insurers to offer packages that they would typically only be able to offer to large corporations. These savings can then be passed on to the small-business clients of the PEO.

PEOs can also help ensure regulations are met. This can be done by providing training, posting safety information, checking job sites for compliance, drug testing, and other measures. In addition, a PEO can help with back-to-work programs or help retrain an injured employee to work in a new position.

The National Association of Professional Employer Organizations provides more details on how PEOs can help with workers’ compensation insurance.

What are the disadvantages of PEO worker’s compensation?

As an employer of record, the PEO should assume liability regarding workplace safety. However, this can be a disadvantage if the PEO is not following the law or if courts determine that the workplace employer also shoulders liability.

In a worst-case scenario, the PEO may not use workers’ compensation insurance recognized by the state the employee works in. Check the certificates provided by the PEO with a list maintained by your state government.

Issues can also come up due to discrepancies in paperwork or human error. There have been cases where it was unclear whether the injured employee was a PEO co-employee or a full-client business employee. In these situations, the client business could be found liable, and if it does not carry workers’ compensation insurance for all non-PEO co-employees, it could also face a fine.

PEO workers compensation: Key advantages

PEO worker’s compensation — our take

Business owners should thoroughly review all contracts, certificates, and insurance documentation to combat the potential disadvantages of PEO-provided workers’ compensation insurance. It should be clear who the co-employees are and what their coverage is.

For a small business requiring a large staff engaged in potentially hazardous work, such as construction or manufacturing, the best PEO could provide reduced and stable premiums, liability protection, and a partner to ensure local regulations are met. For a larger company involved in less dangerous work, such as office work, the benefits of a PEO regarding workers’ compensation insurance may be less.

FAQ

Workers compensation insurance regulations vary from state to state, but it is generally required for companies with more than one employee.

Workers compensation claims are covered by the workers’ compensation insurance provider. Premiums for workers compensation insurance are paid by the employer, not by the employee. If a PEO is providing workers compensation insurance, the client business pays the premiums through the PEO.