![How to Handle National Insurance Contributions [UK Payroll Tax]](https://remotepad.com/wp-content/uploads/2023/02/077da55e-594b-4f5c-83be-a2901977468c.webp)

Table of Contents

showSpending too much on recruitment, payroll or global HR?

We help you find the Best Providers at the lowest cost.

Article roundup

- UK tax law does not use the term ‘payroll tax’, as it is used in the United States. Fulfilling that role in the UK are ‘National Insurance’ contributions.

- National Insurance contributions are a significant compliance and payroll burden for employers and employees alike.

- Businesses should carefully work through the payroll implications of National Insurance for their payroll costs to ensure they have optimized their payment structure.

- As this is a complicated subject area, businesses might consider outsourcing payroll tax/National Insurance management to a payroll company.

In the UK everyone must pay income tax over a certain level. Death and taxes. Not everyone, though, pays National Insurance: Income tax in everything but name, National Insurance is the UK equivalent of what is known as ‘payroll tax’ or ‘employment tax‘ in the US — a tax covering social security and medicare contributions.

Here we look at the difference between income tax and National Insurance in the UK, and explain what businesses need to do to account for this possible tax.

A (very) brief history of National Insurance in the UK

National Insurance is a nimble and cunning tax created at the beginning of the 20th century. If you think Kwasi Kwarteng’s mini budget was controversial in September 2022, read what happened in 1909 with the People’s budget. The then controversial Welsh chancellor (David Lloyd George) with his overenthusiastic sidekick (Winston Churchill), introduced national insurance, surtax, and the welfare state. It triggered a constitutional crisis and ended the dominance of the House of Lords. More importantly, it left all future employees and employers with the burden of national insurance contributions: Payroll tax in everything but name.

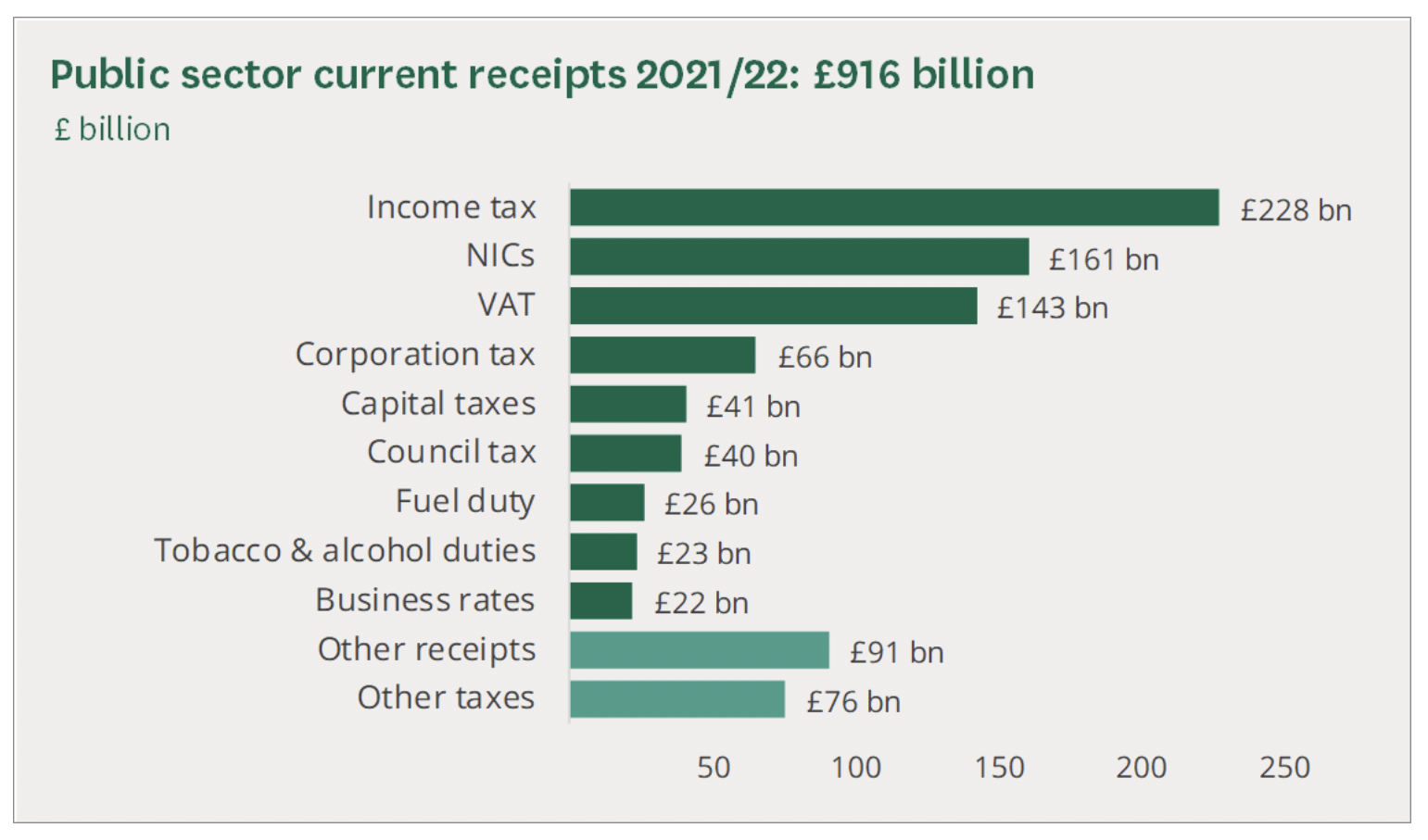

Chart: National Insurance contributions as a proportion of government revenue

In the chart below, courtesy of the UK’s House of Commons library, it is clear that National Insurance makes up a large proportion of the government’s revenue.

Is National Insurance a tax smokescreen?

When Rishi Sunak needed to find more tax in 2021, he turned to National Insurance with a health and social levy of 1.25%. This increased the National Insurance contribution for an employee from 12% to 13.25%. It has since been reversed, but it illustrated a crucial difference in UK taxes.

Take a salary of 50,000 in 2022/23: A normal employee would suffer approximately £7,500 in tax. The payroll software will then also deduct over £4,700 in national insurance leaving a total tax liability to His Majesty’s government of over £12,000. That is a reduction of almost 25% of his total gross pay. Just for a basic rate taxpayer.

But a director and shareholder of a small company has a few options available. They could be placed on the payroll with a gross salary of say £1,000 per month. This would neatly use up a personal allowance. Then they could take out a small loan from the company of under £5,000 with no tax implications or extract earnings above his personal allowance as dividends. If there was sufficient profit, the director and shareholder would walk away with a tax bill of just over £3,100. Using the dividend option reduces a tax burden from 25% to 6%. In other words, being on the payroll can attract 19% more in tax.

The income tax and payroll tax technicalities

Let’s begin with income tax. Every taxpayer in the UK, on or off a payroll (when on-payroll, this income tax is known as PAYE), is entitled to an annual personal allowance which is currently set at £12,570 in 2022/23.

If anyone earns more they must start paying tax. Most countries now apply progressive rate of taxation. In the UK, if you keep your total earnings under £50,000, you are known as a basic rate taxpayer and HMRC are only interested in 20%. Anything above that becomes 40% and as Kwasi Kwarteng (ex-Chancellor of the Exchequer) recently discovered, an extra surcharge of 5% for the highest earners over £150,000 per year is a political necessity.

Payroll software calculators pro-rata the above thresholds, divide them by twelve and apply to each calendar payroll month or cycle. But, unlike national insurance, income tax is cumulative. Every month the payroll software will keep on adding one twelfth of your allowances onto your total earnings to date. If you work only for six months in a tax year, the software will still apply your full annual allowance.

National Insurance: The payroll straitjacket

With National Insurance, though, employees are zipped into the payroll tax straitjacket, well, unless you are a director. For most employees, National Insurance is calculated per payslip. If you receive a fantastic bonus one month and nothing the next, there’s no good looking for a National Insurance refund. It’s gone. No point in relying on a tax return too. Not interested.

An employer is even worse off. At least an upper threshold of £4,189.00 per month exists for an employee, beyond which the percentage drops by 10%. No such luck for an employer. Their 15.05% is fixed for infinity. Moreover, if they provide any taxable benefits such as a company car that attracts even more National Insurance.

Managing your National Insurance/UK payroll tax burden means ensuring 100 percent compliance with your legal and regulatory obligations. If all this is giving you a headache, It may be worth considering how you might outsource your payroll to a payroll bureau.

Expenses and National Insurance

You can also imagine that our director and shareholder may enjoy expenses, a luxury not open to employees. But there is a small quirk in tax law which elevates an employee above the wildest dreams of their owners: a ‘temporary’ workplace. The definition is precise and pertinent. If an employee can ascertain that a particular workplace is only fleeting, a placement for less than two years away from the main office, then they enter the world of expenses.

Suddenly, travelling become deductible, even from home, and subsistence is on the house. Not even the self-employed can enjoy liberty to bill the government from their front door. It is quirk not well known or publicised.

The Covid-19 pandemic advanced the acronym WFH (working from home.) Some employees, for the very first time realised they too can claim back some expenses from the government. Not just the £26 per month government recommended rate of allowance, but capital allowances on equipment or furniture or even a proportion of the electricity bill for a cup of tea!

National Insurance contributions — an explanation from the Institute for Fiscal Studies.

Payroll Tax in the UK — Our Verdict

Before you all resign to become self-employed, I am sorry to say that the government have that covered too. Class 4 National Insurance kicks in above profits of £11,908.00 per annum but instead of 13.25%, they only want 10.25% before you reach £50,000.00. But the crucial word is profit. In payroll tax, National insurance is calculated on total earnings. For the self-employed, the difference is profit. And for our director and shareholder above, National Insurance may not even feature at all.

To sum up, National Insurance is generally a major cost of employment in the UK, is largely equivalent to what is known as payroll tax in the United States (though there are, of course, differences between the two). It is crucial for employers and the self-employed in the UK alike to pay careful attention to National Insurance and how it might contribute to payroll burden.

For businesses unsure about their National Insurance obligations it may be worth getting in touch with a UK Professional Employer Organization or UK Employer of Record (sometimes known as ‘umbrella companies’) to ensure that full compliance.

FAQ

The UK tax regulator, HMRC, does not use the term ‘payroll tax’. Instead, employers are required to pay National Insurance contributions, which are similar to ‘payroll taxes’ — taxes covering social security and medicare contributions — in the United States.

National Insurance contributions in the UK (what US employers would call ‘payroll tax’) are separate from income tax. Employers and employees both contribute to National Insurance, whereas employee income tax (PAYE) is withheld purely from the employee’s gross salary.